Moderators: Elvis, DrVolin, Jeff

![]() by Iamwhomiam » Tue Jul 02, 2019 8:48 pm

by Iamwhomiam » Tue Jul 02, 2019 8:48 pm

![]() by Elvis » Tue Jul 02, 2019 11:23 pm

by Elvis » Tue Jul 02, 2019 11:23 pm

Iamwhomiam » Tue Jul 02, 2019 5:48 pm wrote:Jack, I want to thank you for initiating this thread on the Modern Monetary Theory, and for your contributions to it. Elvis, too, I'd like to thank for adding new, valued content to the discussion. I believe this is one of the most important threads I've read in my years here, though there have been a great many other threads I've read and learned much from. My thanks to you both.

Conclusion

These economists essentially lead sad professional lives. They bunker down in their offices and doodle away with mathematical models that are largely banal representations of some obscure untested assumptions about human behaviour and motivation which the other social science disciplines and relevant research show to be inapplicable.

They lead unadventurous lives – opting to perpetuate conservative myths that are continually violated by the facts. They hide their shame with arrogance.

![]() by Grizzly » Thu Jul 04, 2019 4:11 pm

by Grizzly » Thu Jul 04, 2019 4:11 pm

![]() by Elvis » Thu Jul 04, 2019 5:45 pm

by Elvis » Thu Jul 04, 2019 5:45 pm

Grizzly wrote:There's a good interview with Michael Hudson regarding the World Bank and the IMF at Naked Capitalism today.

ModernMoneyNetwork

Published on Sep 22, 2012

Moderator: William V. Harris, William R. Shepherd Professor of History and Director, Center for the Ancient Mediterranean, Columbia University

Speaker 1: L. Randall Wray, Research Director of the Center for Full Employment and Price Stability and Professor of Economics, University of Missouri-Kansas City

Speaker 2: Michael Hudson, President, Institute for the Study of Long-Term Economic Trends and Distinguished Research Professor, University of Missouri-Kansas City

Tuesday, September 11, 2012

About the Seminar Series:

Modern Money and Public Purpose is an eight-part, interdisciplinary seminar series held at Columbia Law School over the 2012-2013 academic year. The series aims to present new perspectives and progressive policy proposals on a range of contemporary issues facing the U.S. and global macroeconomy. Seminars will feature a mix of academics and practitioners on topics ranging from the history of debt and money and the structure of the financial system to economic human rights for the 21st century.

![]() by Elvis » Thu Jul 04, 2019 7:49 pm

by Elvis » Thu Jul 04, 2019 7:49 pm

Elvis wrote:— People pay more for essential things like healthcare, education, housing, transportation etc; consequently the GDP number goes up, and this is celebrated in the media as "growth."

Hudson notes that the existing economic theory (the Chicago School in particular) is in the service of rentiers and financiers and has developed a special language designed to create the impression that the current status quo has no alternative. In a false theory, the parasitic encumbrances of a real economy, instead of being deducted in accounting, add up as an addition to GDP (gross domestic product) and are presented as productive. Hudson sees consumer protection, state support of infrastructure projects and taxation of parasitic rentier sectors of the economy instead of taxing workers as a continuation of the line of classical economists today.

![]() by JackRiddler » Sat Jul 06, 2019 8:29 am

by JackRiddler » Sat Jul 06, 2019 8:29 am

![]() by Elvis » Mon Jul 08, 2019 9:59 pm

by Elvis » Mon Jul 08, 2019 9:59 pm

https://www.cnbc.com/2019/07/08/read-deutsche-bank-ceo-christian-sewings-email-to-staff-about-job-cuts.html

Read Deutsche Bank CEO’s email to staff about job cuts

Published Mon, Jul 8 2019 2:41 AM EDT Updated Mon, Jul 8 2019 7:33 AM EDT

Spriha Srivastava

Deutsche Bank CEO Christian Sewing, in an email to colleagues, said he “greatly regrets” the impact these job cuts will have on employees, adding that it is in the “long-term interests” of the bank.

Deutsche Bank announced Sunday that it will pull out of global equities sales and trading, scale back investment banking and slash thousands of jobs as part of a sweeping restructuring plan to improve profitability.

Deutsche will cut 18,000 jobs for a global headcount of around 74,000 employees by 2022. The bank aims to reduce adjusted costs by a quarter to 17 billion euros ($19 billion) over the next several years.

Here’s the email that Deutsche Bank’s CEO Christian Sewing sent to staff on Sunday.At the Annual General Meeting in May I said that we would speed-up the transformation of our bank significantly, that we would have to take faster and more radical action. Since then, many of you have asked me when we would announce concrete next steps.

Today is that day: After further stabilizing our bank last year, we are now entering the next phase – and that means nothing less than a fundamental transformation of our bank.

First let me say this: I am very much aware that in rebuilding our bank, we are making deep cuts. I personally greatly regret the impact this will have on some of you. In the long-term interests of our bank, however, we have no choice other than to approach this transformation decisively. Only then can we build on our long-standing history and make Deutsche Bank a leading bank once again. A bank which we can be justifiably proud of.

...

We are creating a bank that will be more profitable, leaner, more innovative and more resilient. It is about once again putting the needs of our clients at the centre of what we do – and finally delivering returns for our shareholders again.

...

And we are not asking our shareholders to pay for this transformation but instead plan to return capital to them.

All of this will create a new, better Deutsche Bank.

However, we also have to face the fact that this transformation will require uncomfortable decisions. This is especially true for the sizeable workforce reductions. I can assure you that my colleagues and I appreciate that this impacts people and affects their lives in a profound way.

...

Taking this decision has not been easy. It has far-reaching consequences for our bank – the bank that I have been working at for almost thirty years now.

But I am determined, and so is my leadership team: This is about thinking radically and thinking differently.

![]() by Elvis » Tue Jul 09, 2019 7:31 am

by Elvis » Tue Jul 09, 2019 7:31 am

Lights Out, Seattle

This story ran in The Seattle Times on Nov. 3, 1996

By Sharon Boswell

and Lorraine McConaghy

Special to The Times

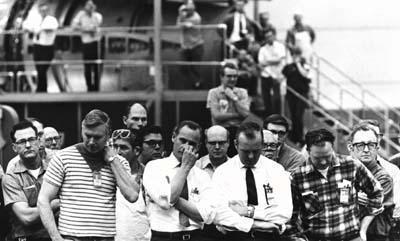

In March 1971, workers at the Boeing Supersonic Transport Division listened to Boeing vice president Lowell Mickelwait announce the final U.S. Senate rejection of funding for the SST program. Photo Credit: Pete Liddell / Seattle Times.

ON NEW YEAR'S DAY 1970, SEATTLE READERS OPENED THEIR TIMES to find the customary annual reviews and predictions. Times guest columnist Miner Baker, president of Seattle-First National Bank, recalled "the Soaring '60s" in which the booming Puget Sound economy "lived up to every promise and then some."

But Baker noted that Boeing's workforce had declined in 1969 to about 80,000 from a 1968 high of more than 100,000; he warned readers that 1970 would be "a painful year of readjustment" to a decade of modest prosperity dependent on the "continued growth in diversified manufacturing."

For 20 years, optimists had claimed a growing industrial versatility, but the region's economic health remained stubbornly pegged to the fortunes of The Boeing Co. In The Times, the biggest news story of 1969 was the introduction of the 747, the world's largest commercial jet. In 1970, the Puget Sound economy was still a one-trick pony; reality would prove far more dire than Baker's forecast.

By late 1971, the Boeing workforce plummeted to 32,500, and local economic indicators were in freefall. Battered by the misfortunes of the area's largest employer and by a national business slump coupled with inflation, the region entered "the longest and deepest recession since the Great Depression," as a Times writer put it in 1975.

In the early 1970s, the U.S. economy was torn between guns and butter, struggling to pay for the Great Society's social programs while waging the war in Southeast Asia. Federal deficit spending rose, as did inflation and interest rates; economic growth slowed and employment fell. Confronted with "stagflation" -- an extraordinary combination of rising prices and economic stagnation -- Richard Nixon's administration cut taxes, raised interest rates and devalued the dollar in quick succession.

Nothing worked, and the energy crisis delivered the final, crippling blow. The world's industrial economy depended on Middle East oil, quadrupling consumption between 1950 and 1970. But in 1973, U.S. military support for Israel prompted the Organization of Petroleum Exporting Countries (OPEC) to embargo crude oil and then to raise prices. Acute shortages of heating oil and gasoline resulted, and the price of crude oil skyrocketed. By 1979, it would cost $30 a barrel.

At home, Boeing sales had soared in the '60s when air carriers eagerly built their fleets of 707s, 727s and 737s, but suddenly there were more seats than passengers to fill them. Sales of the new 747 and the older family of jetliners were slow. In 1970, the company began a 17-month period without a single new order from any U.S. airline. In March 1971, the U.S. Senate rejected further funding to develop Boeing's SST, the supersonic transport with commercial and military applications. Then, the energy crisis hit, driving up the cost of flying.

FIGHTING BANKRUPTCY, BOEING SCALED DOWN TO COMPETE. Growing "lean and mean," as a company spokesman put it, the company laid off 35,000 workers in 1970, another 15,000 the following year. Waves of layoffs rippled through machine shops and industrial suppliers, stores and restaurants. At its height, general Puget Sound unemployment stood at 17 percent. But even after recovery had begun in 1974, Boeing's workforce reached just 54,000 -- half the number of the glory days.

During the Great Boeing Bust, employees waited for the ax to fall, grimly joking that a Boeing optimist brought lunch to work, a pessimist left the car running in the parking lot. By 1972, laid-off machinists, managers, engineers and secretaries had saturated the local job market. Month after month, an avalanche of homes, cabins, powerboats and cars -- at fire-sale prices -- filled The Times' classifieds.

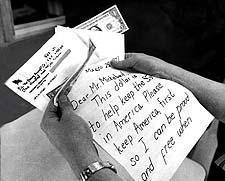

A student's letter was among many sent to Boeing offering sympathy and money for the SST. Nearly $1 million was sent, but returned after the final cut. Photo Credit: Associated Press.

AS THE HARD TIMES CONTINUED, UNEMPLOYMENT BENEFITS WERE EXHAUSTED, extended, then exhausted again; federal food stamps and local Neighbors in Need food banks met basic human needs. Seattle's Crisis Clinic phone volunteers counseled men and women coping with the despair of joblessness. As the area's birthrate fell, the suicide rate rose dramatically; an anti-suicide net was deployed on the Space Needle, and there were calls for a similar safeguard on the Aurora Bridge.

In 1973, a drought brought hydroelectric brownouts, and the ongoing oil crisis forced long waits to buy increasingly expensive gasoline. To a state starved for power, nuclear energy posed an appealing alternative, and the Washington Public Power Supply System (WPPSS) began construction of five nuclear-power plants. But in the mid-'70s, everything still depended on oil.

Consumer prices rose 12 percent in 1974 alone. Local housewives organized a boycott to protest the rising cost of beef, and Seattle-area butchers sold horsemeat roasts and ground buffalo. The Times' Dorothy Neighbors obliged readers with recipes for chili made with buffalo and for cheap, starchy main dishes -- Depression fare.

In 1971, Bob McDonald and Jim Youngren's billboard satirized local gloom-and-doom.

Photo Credit: Greg Gilbert / Seattle Times.

AFTER A GOOD YEAR IN 1972, THE BEAR MARKET OF THE MID-'70S HIT, AND THE DOW JONES INDUSTRIAL INDEX FELL 47 PERCENT IN 1973 AND '74, victim of the inflation-recession double punch. Presidents Gerald Ford and Jimmy Carter met the energy crisis with calls to self-discipline and countered stagflation with an array of tweaks to the economy. But 1980 interest rates stood at nearly 20 percent, inflation was in double digits and unemployment hovered at 8 percent.

Down-sized, Boeing was resurgent by 1980. But the region's fishing, forest, mining, agricultural and shipbuilding industries found it difficult to rebound. For them, economic ills had been compounded by foreign competition, labor disputes and environmental legislation. Few noticed the signs of Seattle's coming high-tech boom; the cost of the 1970s had been too high.

Historians Sharon Boswell and Lorraine McConaghy teach at local universities and do research, writing and oral history. Original newspaper graphics courtesy of the Seattle Public Library.

Laid-off Boeing workers flooded the local job market and crowded state unemployment offices.

Photo Credit: Associated Press.

http://old.seattletimes.com/special/cen ... s_out.html

![]() by JackRiddler » Tue Jul 09, 2019 3:09 pm

by JackRiddler » Tue Jul 09, 2019 3:09 pm

![]() by Elvis » Wed Jul 10, 2019 4:25 am

by Elvis » Wed Jul 10, 2019 4:25 am

Scott Fullwiler

@stf18

a month ago, 25 tweets, 5 min read Read on Twitter

1. Quick(?) MMT 101 lesson:

From the very beginning in the 1990s, MMT has NEVER argued that 'printing money' was necessary. Anyone saying MMT = "print money," even if they (correctly) incorporate an inflation constraint, is getting MMT dead wrong.

2. The argument from the earliest days--@wbmosler 's "Soft Currency Economics," Wray's "Understanding Modern Money," or @StephanieKelton 's "Can Taxes & Bonds Finance Govt Spending?"[read those!]--the MMT argument is that ALL govt deficits are 'printing money' ALREADY (!).

3. These and other foundational, early MMT pieces argue that the choice to issue bonds or not is about monetary policy how to set the CB's interest rate target, not whether to 'finance' a deficit or 'print money.'

4. The argument across literally dozens of publications is consistent--whether or not govt issues bonds when it runs a deficit, the macroeconomic impact of 'bonds vs. money' is nil.

5. What matters for macro impact is the deficit itself, and how it is created (spending/taxing priorities), since the deficit is creating net financial wealth in the pvt sector (note I did NOT say 'real' wealth (!)).

6. The choice to issue bonds or not in the face of a deficit is simply about 1 risk-free govt asset (say, Tbills) vs. another risk-free govt asset of perhaps slightly longer maturity (but that's also a policy choice).

7. This is also partly why we predicted back in the 2001 that Japan's QE wouldn't be inflationary, and predicted the same for the US in 2008. QE & 'monetization' of govt debt is about an asset swap--it's the deficit itself that has the 'quantity' effect, not the financing.

8. Similarly, in the real world, CB's are defending their national payments systems every minute of every day. This means they accommodate banks' demand for CB liabilities always at or near their current interest rate target.

9. From an MMT perspective, it's really weird that people believe a govt running a deficit via overdraft at the CB is inherently inflationary, but the current system, where govt runs a deficit while CB guarantees mkt liquidity for bond dealers to buy govt bonds, isn't.

10. So, from the beginning 20+ yrs ago, MMT said the 'choice' to issue bonds when running a deficit was about how to set CB's int rate target. W/ bond sales, CB accommodates banks at its tgt rate. W/o bond sales, CB sets rate at ZIRP or uses IOR=tgt rate to set tgt rate <> 0

11. This is just supply and demand from ECON 101. If you push out the supply curve beyond the entire demand curve, either the price falls to 0 or you have a price floor set at <> 0. Those are the only 2 possibilities when 'printing money' to run a deficit.

12. Neoclassicals actually agree w/ this, for different reasons. For them, if 'monetize' govt debt & CB rate = 0, 'monetization' isn't inflationary. Or, if CB sets rate <> 0 via IOR=target rate, still not inflationary.

13. In both cases, CB's reserves are considered effectively equivalent to holding, say, Tbills. So, 'monetization' or 'printing money' is effectively equivalent to 'printing' Tbills. IOW, if you blend neoclassical model w/ actual CB ops, 'printing money' isn't inflationary.

14. Putting this all together . . . MMT has NEVER argued that 'printing money' as conventionally interpreted is necessary to carry out MMT policy proposals. All deficits create net financial wealth for pvt sector, regardless of 'finance' method.

15. Choice to issue bonds or not when running a deficit is about how to set CB's target rate, not 'financing' a deficit. This means that interest on national debt is a policy variable, or at least can be (for monetary sovereign, of course).

16. So, choice to issue bonds or not is not about 'quantity' impact of a deficit, but about 'how' CB chooses to achieve its target rate. Hitting interest rate tgt by overdraft to govt & pay IOR=tgt rate=2% has no difference of macro significance from . . .

17. ... hitting interest rate target by govt instead issuing tbills while CB ensures mkt liquidity at tgt rate = 2% to banks & bond dealers.

18. Now, there are places where MMT scholars argued for no bond issuance, govt gets CB overdraft, & CB sets tgt rate= 0 (permanent ZIRP). Note, tho, that this is (a) not arguing in favor of 'printing money' even in neoclassical view (it's Krugman's liquidity trap, actually) ...

19. (b) and is therefore, simply a policy proposal for low interest rates on govt debt. It is also NOT arguing for ZIRP in a neoclassical world--Wray did his Ph.D. under Minsky. Minsky was against manipulating short term rates; instead favored credit regs/margins of safety.

20. That is, when MMT proposes ZIRP, it is proposing it for ONLY the govt debt, NOT for the economy overall as in a New Keynesian model. There are dozens of MMT publications on regulating credit, and more on the way. MMT was about macroprudential before that was a thing.

21. Minsky was adamant that manipulating short-term interest rates was actually destabilizing (he blamed the rise of money manager capitalism on Volcker's high rates). Raise margins of safety to slow credit rather than raising the overnight, risk-free rate.

22. A benefit of margins of safety is that raising interest rates to slow credit leads to higher hurdle rates that can only be met by riskier projects, while raising margins of safety slows credit by favoring the LESS risky loans.

23. Particularly given that the problem of a debt bubble is that credit QUALITY is bad, it's really weird from an MMT perspective that it's mostly MMT arguing in favor of macro policy that target credit quality ...

24. ... while neoclassicals go to lengths to NOT talk about credit quality--use a Taylor rule to manipulate short-term rates, increase liquidity requirements, increase capital, but little to nothing about underwriting. (Shocker--we now have a corp debt bubble.)

25. So, MMT is NOT arguing for 'printing money' and 'ZIRP' in the conventional, neoclassical world. MMT is arguing for stabilizing demand side of the economy w/ a mix of govt's budget position (at low rates, however 'financed') & credit quality/margins of safety.

![]() by Elvis » Thu Jul 11, 2019 8:47 pm

by Elvis » Thu Jul 11, 2019 8:47 pm

Deep in contraction:

Looks to be below 2008 levels:

So looks like the current tariffs remain. As previously suggested, the US President is narrowly focused on the money he’s collecting, as the tariffs remove $US net financial assets from the global economy and discourages transactions with the US. That is, it all functions as a transactions tax on the global $US economy

http://moslereconomics.com/2019/06/29/r ... rade-news/

![]() by Elvis » Fri Jul 12, 2019 1:03 pm

by Elvis » Fri Jul 12, 2019 1:03 pm

Interest Rates Just Keep Falling. Economic Orthodoxy Is Falling With Them.

Investors expect even lower growth and inflation; this isn’t the way it’s supposed to work.

By Neil Irwin

July 4, 2019

American borrowing costs keep plunging, and that is signaling something important: Some of the basic assumptions of the most influential economic technocrats in the land are, for the time being at least, off base.

Ten-year United States Treasury bonds are yielding only 1.95 percent, down from around 2.4 percent in May and 3.2 percent as recently as November. Global investors are essentially flinging money at any creditworthy entity that might wish to borrow. Rates on home mortgages, corporate bonds and the debt of countries around the world have been falling as well.

This is terrific news if you are a homeowner thinking of refinancing your mortgage or a chief financial officer about to roll over some of your company’s bonds. It is terrible news if you want to see faster global economic growth in the years ahead. Lower long-term rates imply that investors expect even lower growth and inflation than had seemed probable just weeks ago.

But there is a bigger lesson in falling long-term interest rates — especially coming at this point in the economic cycle, amid this mixture of tax and spending policies coming from Washington.

Consider some of the assumptions that are embedded in the economic models of the two government agencies most respected for their independence and technical expertise: the Congressional Budget Office and the Federal Reserve.

When the C.B.O. projects how legislation will affect the economy, it assumes that when the government borrows more, higher deficits will cause interest rates to rise, crowding out investment by the private sector.

Generations of college economics students have been taught that this is simply how things work, and the reason that countries should avoid running large budget deficits. But the logic just isn’t holding up right now.

For example, in the spring of 2018, when the C.B.O. modeled tax cuts and spending increases that had been agreed to the preceding winter, it forecast that higher deficits would result in higher interest rates: 3.7 percent on 10-year Treasury bonds in 2019.

That is 1.75 percentage points higher than actually was the case on Wednesday.

In 2015, the budget deficit was 2.4 percent of G.D.P., a number that is on track to rise to 4.2 percent this year. Yet the 10-year bond yield is now comfortably below its average level in 2015, which was 2.14 percent.

Low interest rates worldwide are probably a factor. Global investors find Treasury bonds appealing because they offer better returns than equivalent securities in Europe or Japan, even after the recent drop in rates. The implication is that higher deficits haven’t come with the costs that economic orthodoxy predicted.

Meanwhile, the Federal Reserve has raised interest rates — albeit in fits and starts — since the end of 2015 based on its own form of economic orthodoxy. It’s the idea that as unemployment falls, eventually it will cause an outburst of inflation — so part of the job of a central bank is to raise interest rates pre-emptively to slow the economy in time to prevent unemployment from falling too far.

At the meeting in December 2015 where Fed officials first raised rates, for example, their consensus projection was that the longer-term level of the unemployment rate was 4.9 percent and that they would need to raise interest rates to 3.5 percent by now to keep the economy in balance and forestall inflation.

The actual results have undermined those assumptions. The unemployment rate has fallen to 3.6 percent. But the inflation rate has remained persistently below the 2 percent the Fed aims for. If anything, the growth rate of workers’ wages has been slowing in recent months. That’s important because higher wage growth is, in the traditional theory, the mechanism by which a tight labor market fuels overall inflation.

Moreover, the movements in bond markets the last few weeks suggest that very low inflation is likely to be the norm indefinitely, despite the low jobless rate. Prices of inflation-protected bonds versus regular bonds imply that consumer prices will rise only 1.66 percent a year over the coming decade.

And rather than raise rates to 3.5 percent, as Fed officials in 2015 envisioned, they have raised their main interest rate target to only about 2.4 percent — and now are poised to cut it in the near future as the world economy starts to creak.

Global factors are a major driver of the disconnect. The United States economy has been relatively strong in recent years compared with Europe and Japan, but the slow growth in much of the world has acted on a brake on how much the Fed can raise rates and how much inflation can emerge.

When rates in the United States rise too high relative to other major economies, the dollar strengthens on global currency markets, which then weakens American export industries. Tighter money in the United States can send ripples to emerging markets where many companies borrow in dollars — meaning that when the Fed raises rates, it can slow the entire global economy, and worsen already powerful deflationary forces.

There have been moments over the last few years when the old economic rules were reasserting themselves — when it seemed that high deficit spending really was starting to push interest rates higher, and when low unemployment was starting to fuel a cycle of higher wages and prices.

They have turned out to be false dawns. A set of rules that seemed to describe how the world works as recently as 2007 seems to have given way to something different. We now have a complex set of challenges, including an aging work force, that can’t be easily turned around.

The first step, though, is for all those in a position to influence economic policy to ask deep questions about whether what they learned in a college economics classroom all those years ago might no longer be so.

The Fed’s New Message: The Economy Can Get a Lot Better for Workers

A rejection of what had been a consensus view of the relationship between the jobless rate and inflation.

By Neil Irwin

July 11, 2019

Jerome Powell testifying Wednesday at a hearing on Capitol Hill. “To call something hot, you need to see some heat,” he said of the labor market.CreditZach Gibson/Getty Images

Sometimes, ideas can bounce around the intellectual fringes for years before eventually being embraced by the powerful. On Wednesday you could watch it happen in real time, on cable television.

In congressional testimony, the Federal Reserve chair, Jerome Powell, argued that despite the low unemployment rate, the job market was not yet in an all-out boom and that there was room for further improvement without worrying too much about inflation. He even hinted that American workers were due for some catch-up growth in their compensation — after years in which their pay fell as a share of the economy.

It was implicitly a rejection of what had been a consensus view among leaders of the central bank as recently as last year: that the economy had already achieved, or was quite near to, full employment, and therefore that the Fed needed to raise interest rates to prevent inflation.

Consider some of his remarks during his appearance Wednesday before the House Financial Services Committee.

“We don’t have any basis or any evidence for calling this a hot labor market,” Mr. Powell said. “We haven’t seen wages moving up as sharply as they have in the past.”

“To call something hot, you need to see some heat,” he added, as pithy a statement of economic conditions as you’ll hear from a Fed chief.

Representative Alexandria Ocasio-Cortez, Democrat of New York, later asked, “Do you think it’s possible that the Fed’s estimates of the lowest sustainable unemployment rate may have been too high?”

“Absolutely,” Mr. Powell replied, adding that the Phillips curve, the statistical relationship between low joblessness and higher inflation that has been central to Fed policymaking for decades, is showing itself as but a “faint heartbeat.”

He repeatedly noted evidence that the low jobless rate had led employers to be more willing to hire less qualified workers and spend money training them — a phenomenon with big potential longer-term benefits for both those people and the economy as a whole.

Perhaps most revealing, he seemed open to the possibility that workers should reclaim a higher share of the nation’s economic output.

Representative Denny Heck, Democrat of Washington, said, “Why hasn’t the Fed called out more than a generation of lack of wage growth?”

“Go back to the turn of the century: What you saw was a decline in the labor share, and that has not been reversed,” Mr. Powell said, using a term for the share of national income that goes to workers in the form of pay and benefits.

“We’re missing 10 years of growth,” he continued. “I think that’s really the underlying problem. We’re getting reasonable wage growth, but we missed all of those years beginning at the beginning of the century. It’s a very serious problem, and we should do a better job of calling it out.”

By contrast, not long ago, Mr. Powell and other leaders of the central bank were proceeding on the assumption that the job market did not have room to get much better without setting off an inflationary spiral.

In a 2017 speech, for example, when he was a Fed governor, Mr. Powell said that estimates of the long-term rate of unemployment indicated that “the unemployment rate gap has essentially been closed” and that “a variety of other measures also suggest that we are close to maximum employment.”

The unemployment rate was 4.7 percent that month, and it has fallen a full percentage point since, with no evident rise in inflation.

So what has changed? The simplest answer is: the data.

It may have been plausible two or three years ago to think it was only a matter of time before a tight job market translated into more rapidly rising compensation for workers, and, in turn, broader inflation. But it hasn’t happened, or at least not remotely to the degree that those models predicted.

It probably also helps that the Fed is now under pressure, from both conservatives and liberals, to increase economic growth. That gives Mr. Powell room to speak of improving conditions for workers without coming across as partisan.

Trump administration officials, particularly the National Economic Council chief, Larry Kudlow, have argued that there is no reason to think a stronger job market will stoke inflation. And the president has criticized Mr. Powell and the Fed for last year’s interest rate increases.

The shift also comes after years in which a handful of voices in the relative wilderness, both inside and outside the central bank, have been building the intellectual case for the view that Mr. Powell embraced Wednesday.

Internally, the Minneapolis Fed president, Neel Kashkari, has made arguments along these lines for years.

Outside the central bank, the activist group Fed Up has contended since its formation in 2014 that the economy was not as close to health as many Fed officials assumed, and that the Fed should forestall interest rate increases until there was more widespread prosperity.

A range of economists has also made these arguments, though often not the boldface names of the profession, but younger academics less tethered to an orthodoxy that dates back decades.

“I wouldn’t say we have won yet, but we are definitely making progress,” said J.W. Mason, an assistant professor at John Jay College at City University of New York who has written on these ideas. “Compared with a few years ago, the debate has definitely shifted in favor of those of us who have been saying that there is much more slack in the economy than conventional measures suggest, and that macroeconomic policy has been systematically too conservative — too worried about inflation and not worried enough about unemployment.”

This hasn’t been an overnight shift. You can see in comments from a range of top Fed officials over the last couple of years that they have grappled with the possibility that they have been overly confident in their assessment that the economy was closing in on full health.

But Mr. Powell’s appearance before Congress on Wednesday should leave little doubt of where the intellectual currents are flowing.

![]() by Elvis » Fri Jul 12, 2019 1:55 pm

by Elvis » Fri Jul 12, 2019 1:55 pm

https://www.npr.org/podcasts/381444600/marketplace

July 11, 2019

What it really means when legislation "pays for itself"

![]() by PufPuf93 » Fri Jul 12, 2019 3:37 pm

by PufPuf93 » Fri Jul 12, 2019 3:37 pm

Elvis » Tue Jul 09, 2019 4:31 am wrote:BOEING BOEING

Related the present layoffs—from 50 years ago. Also personal: in 1971, after 22 good years as a Boeing engineer, my father, who had gone West for the 1960s aerospace Boom, was laid off. It was not unexpected; for more than a year a gloomy pall had hung over the entire "Lazy B" workforce as pink slips—randomly selected layoff notices—were handed out daily to meet quotas.

The consequences of that one layoff alone out of thousands—sudden joblessness, upheaval, loss of "dream home," moving around, divorce, debt, despair—are pretty typical and could have been averted with a federal fucking job guarantee (FFJG).

Eventually—like over two fucking years later—too late to fix much of the damage—Congress got around to passing the Comprehensive Employment and Training Act, CETA. My father was selected and duly dispatched to Berkley for accelerated courses in civic management. His travel, accommodations (a dorm apartment), meals and tuition were all paid by the federal program which even included a stipend.

While "comprehensive" a more than generous characterization, CETA changed everything. A neat feature of the Act was that it provided its graduates with a job—a federally funded job. My father was made "Federal Programs Coordinator" whose job at a suburban school district was to submit applications to the federal government for (naturally) federal funds. The inflow of federal funds, badly needed in the midst of thousands of layoffs, made my dad a hero in the district offices and he was soon put running the show as superintendent. (It was at this time my father gave me his copy of Nixon's soon-suppressed National Commission on Marihuana and Drug Abuse report which so impressively exonerated cannabis. Copies had been sent to school administrators before Nixon could stop further publication. I think I lost the book many years ago, I can't find it now.)

CETA did what it set out to do, and one reason it was successful to the extent it was, was it left decisions about the application of the funds to local administrators who knew best what was needed in a community. But it was like a band-aid applied too late to a wound that won't ever heal by itself.

It might make a good movie: Nerd gets good engineering job, moves up, everything great for 20 years. Economy sags, Nerd now jobless in high-inflation recession (huh?)—can't find job, loses house, wife separates, kids rotten; friends, relatives and unemployment benefits help. At night Nerd clutches bourbon—not scotch—listening to Streisand on stereo. Act III: Letter comes, CETA to the rescue! Nerd gets new career, new wife, new house, waves as CETA rides into sunset, the Comprehensive Employment and Training Act to be replaced by the Workforce Innovation and Opportunity Act. (I'm not making that up.)

I played the spoiled teenager in that movie and I think the storyline sucked. The plot would have been better with less drama. And anyway, it's a tired, old story that didn't need retelling.

The fate of CETA recalls the 1946 Full Employment Act, which was, as the name says, a firm commitment to full employment. Thus it was never made into law. Big business saw to that. Instead, it got watered down to the shorter-to-say and commitment-free Employment Act of 1946. "Its main purpose was to lay the responsibility of economic stability of inflation and unemployment onto the federal government." It was bullshit.

I say the Workforce Innovation and Opportunity Act is bullshit, too. Expenditures of $26 billion over the 2014-2018 period as the "primary federal workforce development legislation" is bullshit.

I didn't intend to write a story here, but just today I connected my MMT revelations to my own experience, when I went to look up some statistics. With a fresh 'MMT' perspective on 1971 (and just reading about it in Galbraith), I was curious how many Boeing personnel were laid off in those days. So, Googled and found this 1996 Seattle Times recollection, it describes the "pink slip" pall of gloom to a tee, and I remember the famous billboard: "Will the last person leaving Seattle - turn out the lights."

Users browsing this forum: No registered users and 13 guests