Moderators: Elvis, DrVolin, Jeff

![]() by drstrangelove » Fri Jan 14, 2022 12:07 am

by drstrangelove » Fri Jan 14, 2022 12:07 am

![]() by drstrangelove » Sat Jan 15, 2022 8:00 am

by drstrangelove » Sat Jan 15, 2022 8:00 am

![]() by drstrangelove » Tue Jan 18, 2022 9:19 pm

by drstrangelove » Tue Jan 18, 2022 9:19 pm

![]() by drstrangelove » Sat Jan 22, 2022 7:06 pm

by drstrangelove » Sat Jan 22, 2022 7:06 pm

![]() by MacCruiskeen » Sat Jan 22, 2022 7:39 pm

by MacCruiskeen » Sat Jan 22, 2022 7:39 pm

![]() by drstrangelove » Sat Jan 22, 2022 7:50 pm

by drstrangelove » Sat Jan 22, 2022 7:50 pm

![]() by MacCruiskeen » Sat Jan 22, 2022 7:59 pm

by MacCruiskeen » Sat Jan 22, 2022 7:59 pm

![]() by Joe Hillshoist » Sat Jan 22, 2022 9:43 pm

by Joe Hillshoist » Sat Jan 22, 2022 9:43 pm

drstrangelove » 23 Jan 2022 09:50 wrote:I'd buy an NFT of the NIST modelling which proved WTC 7 free fall collapsed due to fires in silico.

![]() by drstrangelove » Mon Jan 24, 2022 1:54 am

by drstrangelove » Mon Jan 24, 2022 1:54 am

![]() by JackRiddler » Mon Jan 24, 2022 9:35 am

by JackRiddler » Mon Jan 24, 2022 9:35 am

drstrangelove » Mon Jan 24, 2022 12:54 am wrote:in tandem with what could possibly develop into a little bit of a soft shooting war with Russia

![]() by Harvey » Mon Jan 24, 2022 10:40 am

by Harvey » Mon Jan 24, 2022 10:40 am

![]() by drstrangelove » Mon Jan 24, 2022 10:57 am

by drstrangelove » Mon Jan 24, 2022 10:57 am

![]() by Belligerent Savant » Mon Jan 24, 2022 12:25 pm

by Belligerent Savant » Mon Jan 24, 2022 12:25 pm

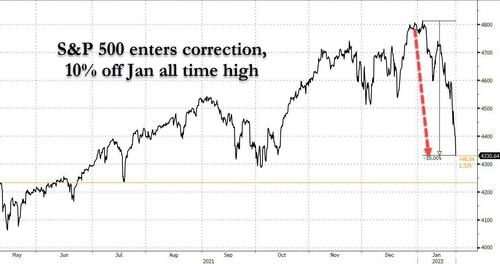

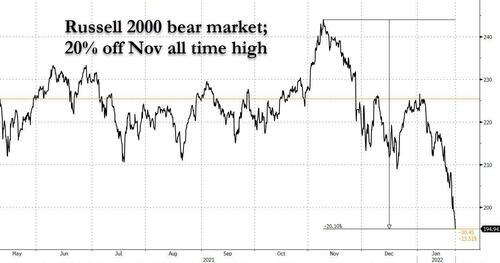

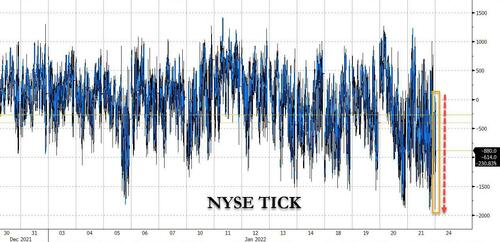

Capitulation Bloodbath: Stocks Crash After Most Negative Opening TICK Of 2022, Russell Enters Bear Market As VIX Explodes

MONDAY, JAN 24, 2022 - 10:02 AM

It's official: as of this morning, the S&P is in a correction, having tumbled 10% from its all time high recorded at the start of the month...

with the Russell suffering an even more humiliating fate, as it entered a bear market at roughly the same time, tumbling 20% from its early November all time high.

The opening puke was precipitated by a marketwide flush, manifesting in the most negative opening TICK in a year at -1,897...

which was also the 2nd most negative TICK of 2022 as everyone hit the sell button at the same time.

And as stocks (and cryptos) crash, and yields tumble, the VIX is exploding above 35, the highest since Jan 2021, and the level which DataTrek said would likely mark the bottom in sentiment.

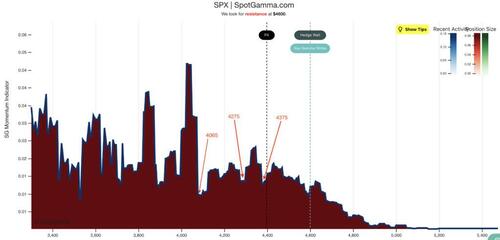

Commenting on today's market technicals, SpotGamma writes that Fridays expiration leads to a reduction in gamma, but we still anticipate high volatility for today. Resistance is at 4400 followed by 4453. Support lies at 4356 and 4330. We are now clearly below both supports.

As SG warns, "This is a very fragile, unstable market which is likely prone to large, directional swings" and continues:As there was a substantial expiration on Friday, we expect that many hedges need be settled across indicies and single stocks. Based on this we anticipate some opening chop due to these hedge adjustments. For example TSLA, which had nearly $20bn in call deltas expiring Friday, is quoted in premarket trading at ~$900 (-4.5%)

However, we generally believe that the expiration of large put options can lead to a short cover rally in markets. Due to large negative gamma position, we think these rallies could be violent, but offer little stability and could mean revert quickly.

Echoing Goldman, SpotGamma notes that it does not think there can be a material rally in stocks until after Wednesdays FOMC. Aside from investors waiting to assess various policy implications, its likely that traders are hedging the event which will hold implied volatility high. This limits the positive vanna flows that could enter the market.

With this in mind, both short dated S&P options & the VIX are at 30 which implies a 1.8% 1 day move. This places the term structure in a backwardated position, which suggests a fair amount of fear in markets. Again, given the FOMC, we think that traders may look to sell very short dated “pre-FOMC” IV which could provide a brief market tailwind, too.

And with stocks taking out low after low, SpotGamma cautions that there are essentially 2 zones for support. One is at 4275, and the other is well south at 4080. If traders elect to initiate new put positions that would pressure markets lower, and increase elevated IV levels. This could accelerate the velocity of any downside move.

![]() by Pele'sDaughter » Mon Jan 24, 2022 1:54 pm

by Pele'sDaughter » Mon Jan 24, 2022 1:54 pm

NEW YORK (AP) — The Dow Jones Industrial Average has dropped more than 1,000 points Monday as financial markets buckled in anticipation of inflation-fighting measures from the Federal Reserve and the possibility of conflict between Russia and Ukraine. Stocks extended their three-week decline on Wall Street and put the benchmark S&P 500 on track to close in what the market considers a correction — a drop of 10% or more from its most recent high. Just after noon, the Dow was down 2.9% while the S&P 500 dropped 3.6%. The Russell 2000 index of smaller companies, whose fortunes are more closely tied to the domestic economy, is now down more than 20% from its recent high.

Stocks sank in morning trading on Wall Street Monday, putting the benchmark S&P 500 on track for what the market considers a correction — a drop of 10% or more from its most recent high.

The S&P 500 fell 2.5% to 4,287.22 as of 10:15 a.m. Eastern, and is now down about 10.7% from the high it set on Jan. 4. A close of 4,316.90 or lower will put it into a correction.

The declines in the market extend a recent run of losses that have left major indexes in a January slump. The Dow Jones Industrial Average fell 712 points, or 2.1%, to 33,544 and the Nasdaq fell 3%.

[....]

The Fed’s benchmark short-term interest rate is currently in a range of 0% to 0.25%. Investors now see a nearly 70% chance that the Fed will raise the rate by at least one percentage point by the end of the year, according to CME Group’s Fed Watch tool.

Federal Reserve policymakers will release their latest statement on Wednesday.

On Monday, the energy and raw materials sectors lead the decline. Mining concern Freeport McMoRan slipped 4.6% and General Motors fell 4%.

Technology stocks were among the heaviest weights on the market as investors shift money away from pricier stocks in anticipation of rising interest rates. Higher rates make shares in high-flying tech companies and other expensive growth stocks relatively less attractive.

Apple fell 1.7% and Microsoft shed 1.8%.

A wide range of retailers, travel-related companies and others that rely on direct consumer spending also fell broadly and weighed down the broader market. Target fell 1.1% and Carnival fell 5%.

Bond yields edged lower. The yield on the 10-year Treasury fell to 1.72% from 1.74% late Friday.

Falling yields also weighed on banks, which rely on higher yields to charge more lucrative interest on loans. Bank of America fell 3.8%.

[....]

Rising costs are raising concerns that consumers will start to ease spending because of the persistent pressure on their wallets.

Investors are monitoring the latest round of corporate earnings, in part, to gauge how companies are dealing with higher prices and what they plan to do as inflation continues pressuring operations.

Monday is a relatively quiet day for earnings, but the pace picks up on Tuesday with American Express, Johnson & Johnson, and Microsoft reporting results. Boeing and Tesla report their results on Wednesday. McDonald’s, Southwest Airlines and Apple report results on Thursday.

Wall Street also has several key economic reports to look forward this week. Investors will get more data on how consumers feel with the release on Tuesday of The Conference Board’s Consumer Confidence Index for January. The Commerce Department releases its report on fourth-quarter gross domestic product on Thursday and its report on personal income and spending for December on Friday.

![]() by Wombaticus Rex » Mon Jan 24, 2022 6:23 pm

by Wombaticus Rex » Mon Jan 24, 2022 6:23 pm

Perhaps the most important longer-term negative of these three bubbles, compressed into 25 years, has been a sustained pressure increasing inequality: to participate in the upside of an asset bubble you need to own some assets and the poorer quarter of the public owns almost nothing. The top 1%, in contrast, own more than one-third of all assets. And we can measure the rapid increase in inequality since 1997, which has left the U.S. as the least equal of all rich countries and, even more shockingly, with the lowest level of economic mobility, even worse than that of the U.K., at whom we used to laugh a few decades back for its social and economic rigidity. This increase in inequality directly subtracts from broad-based consumption because, on the margin, rich people getting richer will spend little to nothing of the increment where the poorest quartile would spend almost all of it.

So, here we are again. This time with world record stimulus from the housing bust days, followed up by ineffably massive stimulus for Covid. (Some of it of course necessary – just how much to be revealed at a later date.) But everything has consequences and the consequences this time may or may not include some intractable inflation. But it has already definitely included the most dangerous breadth of asset overpricing in financial history. At some future date, when pessimism rules again as it does from time to time, asset prices will decline. And if valuations across all of these asset classes return even two-thirds of the way back to historical norms, total wealth losses will be on the order of $35 trillion in the U.S. alone.5 If this negative wealth and income effect is compounded by inflationary pressures from energy, food, and other shortages, we will have serious economic problems.

Users browsing this forum: No registered users and 14 guests